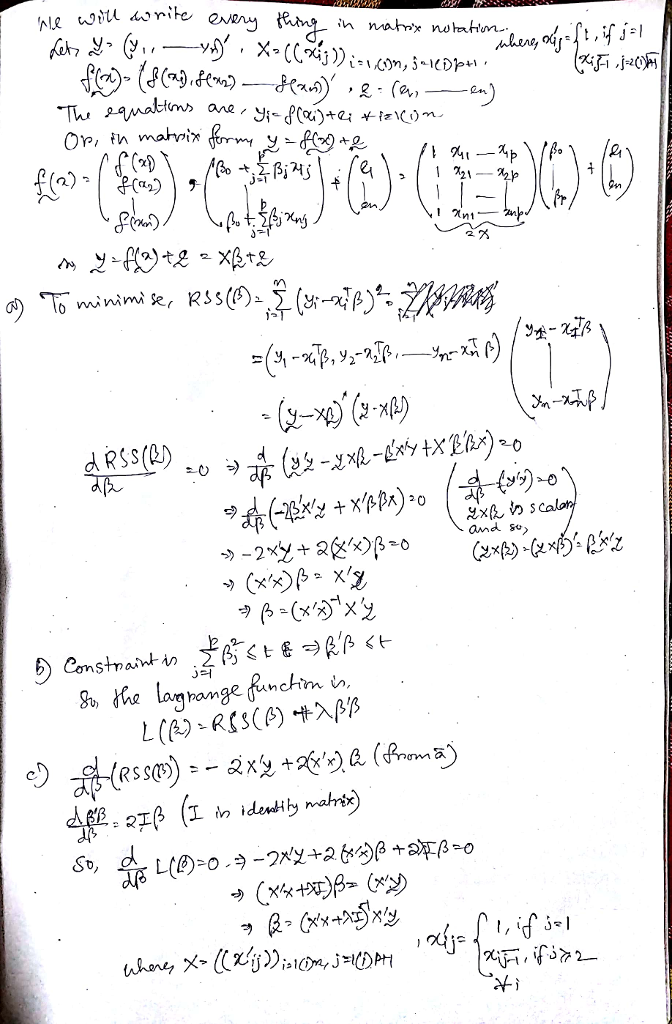

Suppose we observe a training set

{Dox-(1,ail,rar . . , rip)) for i-l, m ,n subjects. We want to fit a linear

regression model /(x) otXI ,, to the training data to minimize the residual sum

ofsquares RSS(β) Σǐ 1 (Vi r β)2 where β = (A 屆,-. W pm (a)(10%) Please

derive the solution ßt. arg ming RSS(β) in terms of Y-|h li) Ar (b)(10%) in

ridge regression, we find ßridge rgminß RSS(β) subject to Σ./ Please write out

the equivalent Lagrangian form of the optimization problem. st. (c) (10%)

Please derive the form of ßridge in terms of Y # (yī and the Lagrange

multiplier λ YnF, X x(zh t

ANSWER

Comments

Post a Comment